So I saw this post on Instagram, and I've a few thoughts to share

-

So I saw this post on Instagram, and I've a few thoughts to share:

Anthony DePice🐺 • #StopCopCity🐢 on Instagram

2,606 likes, 14 comments - j.anthony.depice on October 26, 2024

Instagram (www.instagram.com)

-

So, firstly, yes, I absolutely agree with that post. It's absolutely correct, and we can do better in society.

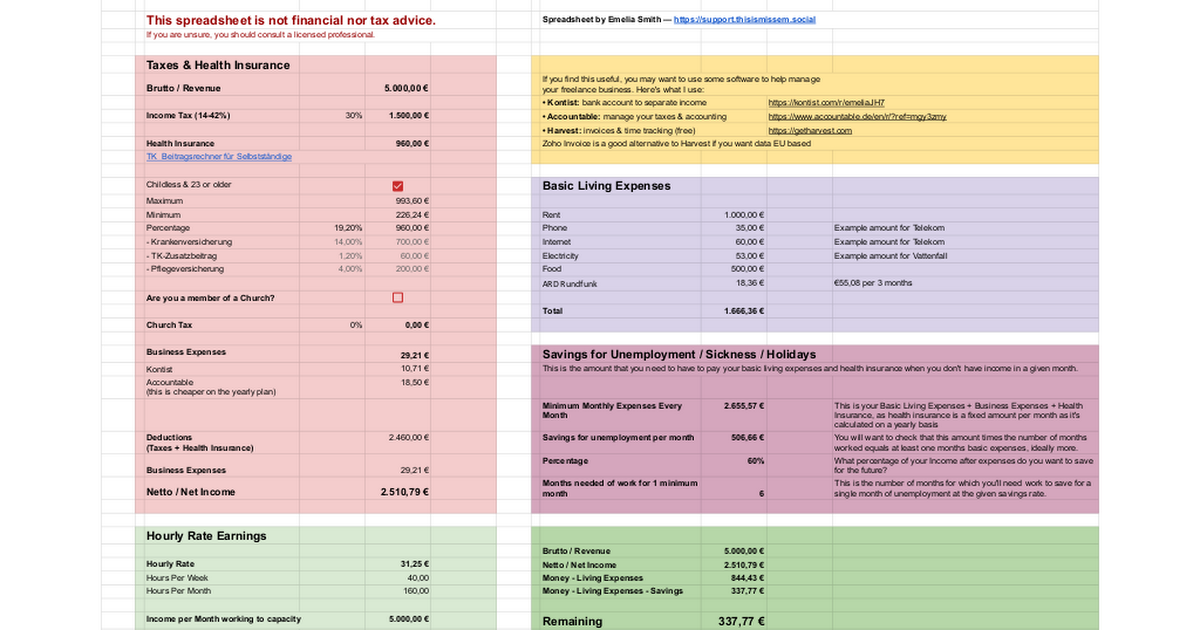

Earlier this year I shared a simple calculator that I use to help figure out financial viability for #freelancers, after several members of International Women Berlin were trying to figure out freelancing.

(Eventually I'll write a web version of this instead of excel/google sheets)

-

Anyway, one of the biggest questions I received on that was "why is there a section for 'savings for unemployment, holidays and sick leave'?"

And the answer is pretty simple: as a freelancer, it can be pretty easy to live the high life when on a good contract and then to struggle when that ends.

Time not working is usually money not earned, so it's really important to have that buffer zone in your financial planning.

-

Emelia 👸🏻replied to Emelia 👸🏻 last edited by [email protected]

As a personal example of this, building that buffer has been really difficult for me at the moment, as I'm only just reaching the "break even" point for the work I'm doing on the fediverse.

At the moment I'm barely covering expenses.

Last year, I *spent* €16,000 to do the work that I did. Yes, you read that right, I made a loss of €16k in 2023

-

However, I'm also somewhat lucky in that most of my income doesn't directly correlate to time input at the moment: folks support my work on the Fediverse on a monthly basis, regardless of my time input.

This is incredibly rare & skews me more towards "creator" than "freelancer" (though creators are of course freelancers)

But this does mean I've managed to weather 40 days of sick leave reasonably well, whilst I waited for my recent heart surgery & the recovery afterwards.

-

Do I want to get back to a point of having cash reserves and a financial safety net? Abso-fucking-lutely.

Last November I was actually so far in the hole that I had a major depressive episode and had to ask someone I knew to help pull me up out of it.

(She later became my partner & dominant, which is super cute!)

But yeah, when freelancing, know your deductions from pay (taxes, health insurance) and know a rough monthly budget.

Then use that to save towards a buffer.

-

Addendum: along with eventually writing a web version of that spreadsheet, I also want to write a web version of how I manage my personal finances:

It's basically based around the idea of amortisation.

So like if I have a bill that's due once every three months, e.g., tv & radio tax, and let's say that's €55 each time.

In my spreadsheet, it calculates how much I need to put aside each month to have money together to pay that future bill.

So I'll save €18,34 each month towards that.

-

That way when that €55 bill gets debited on my account, I'm fine because I just move the money back from my savings for bills.

So each month it's like I only pay €18,34, not that every 3 months I have an unexpected €55 bill

-

Anyway, if you liked this thread or the spreadsheet & ideas, feel free to financial support my work.

The more supporters I have, the better I can weather storms like suddenly requiring heart surgery this month.

Support Emelia Smith (@thisismissem)

Fund her work on the Fediverse, improving trust & safety and other open-source contributions

(support.thisismissem.social)

-

@thisismissem I don't know if this is too US/$-centric and maybe I've already mentioned it before, but https://cushionapp.com/ tries to help with that as well. Originally put together by @destroytoday, and (as far as I know) still maintained by him and a few others.

-

@jochie @destroytoday that's neat, hadn't seen this before, I mostly just put this together out of need